Social Security claiming

Claim at 62, 67, or 70? See the trade-off, side by side.

Claim Social Security early and you get a smaller check for more years. Wait, and you get a bigger check for fewer. The break-even age is simply when waiting finally adds up to more total dollars — and it depends on your benefit, your spouse, and how long you expect to live. GlidePath Money lays out 62 vs 67 vs 70 in plain English so you can see the tradeoff for yourself.

It shows the math — the monthly checks, the lifetime totals, the spousal and survivor math — and it explicitly doesn’t tell you when to claim. That decision is yours (ideally with a fiduciary).

What “break-even age” actually means.

It’s the moment the math flips — and it’s simpler than it sounds.

Say your full-retirement benefit is at age 67. Claim at 62 instead and the check is permanently smaller — but it starts five years sooner, so you bank a head start of payments. Wait until 70 and the check is much larger, but you collected nothing in the meantime. The break-even age is when the bigger-but-later checks finally catch up to and pass the smaller-but-earlier ones in total dollars received.

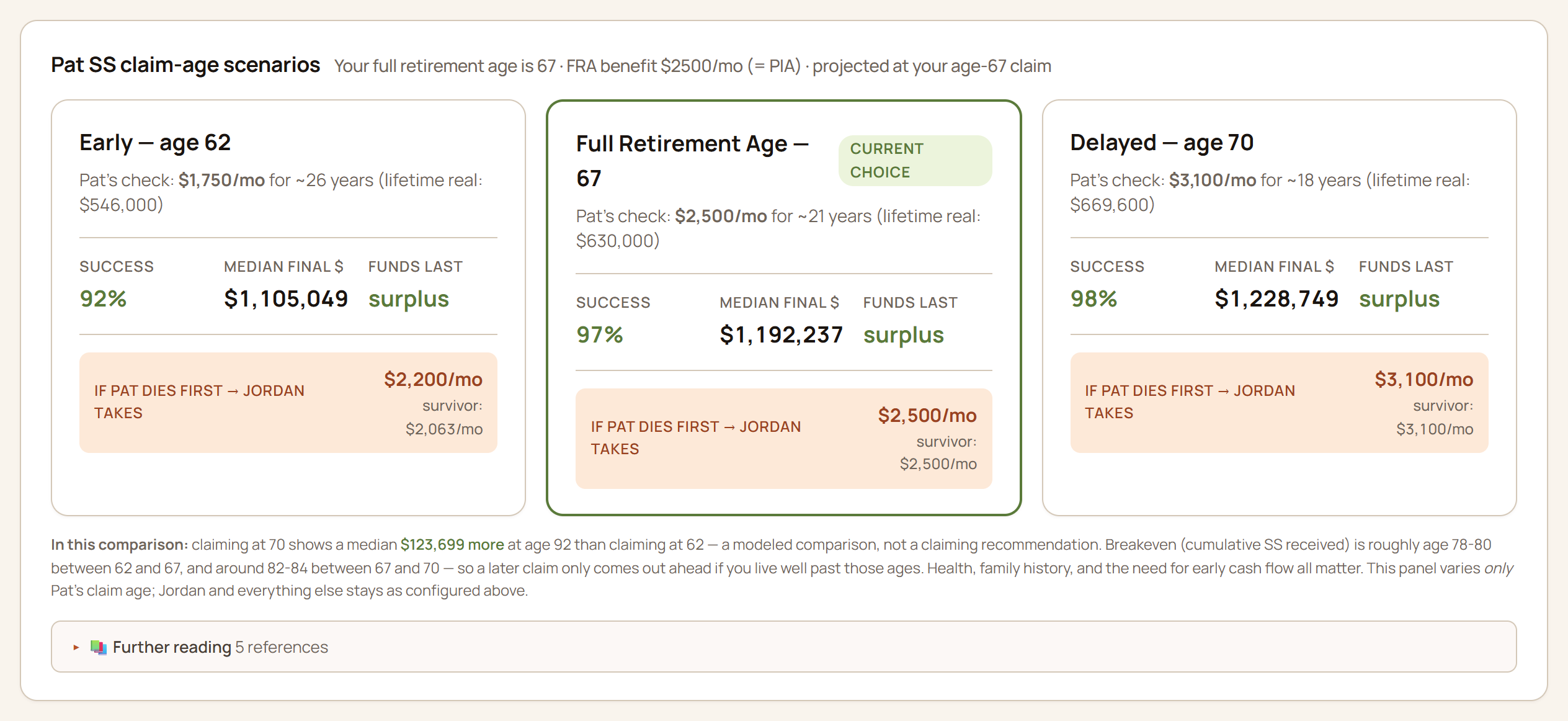

As a rule of thumb that crossover lands somewhere in the late 70s between claiming at 62 and 67, and around the low 80s between 67 and 70. So a later claim only comes out ahead on cumulative dollars if you live well past those ages — which is why your health, family history, and whether you need the cash flow sooner all matter. There’s no single right answer, only the right answer for your situation.

Each claim age as its own card: the monthly check, the years you’d collect, the lifetime real-dollar total, and how the plan holds up — computed on your own machine.

The app surfaces the lifetime totals and the general break-even ranges — it never picks an age for you.

What the comparison actually computes.

Three claim ages, side by side

GlidePath runs your benefit at 62, 67, and 70 as three cards. Each shows the monthly check, roughly how many years you’d collect, and the lifetime total in today’s dollars — so the early-and-smaller vs. later-and-bigger tradeoff is right in front of you.

Each age, run through your whole plan

A claim age isn’t just a benefit number — it reshapes your retirement. Each card also shows that age’s Monte Carlo success probability (out of 1,000 simulated market futures), its median ending balance, and how long your funds last. Same plan, three claim ages, three outcomes.

Spousal & survivor math, for couples

If you’re married, GlidePath models the spousal benefit (up to half the higher earner’s full amount) while you’re both alive, and the survivor benefit one of you would step up to if the other passes first — reduced for an early claim, the way the SSA rules actually work.

Your full retirement age, figured out for you.

“Full retirement age” (FRA) is the age you get 100% of your benefit — no early reduction, no delayed bonus.

It isn’t the same for everyone. GlidePath derives your FRA from your birth year: 67 for anyone born in 1960 or later, and 66 plus a few months for the 1955–1959 cohorts who are still actively choosing a claim age. The 62 / 67 / 70 cards are labeled against your real full age, so “early,” “full,” and “delayed” mean what they should for you specifically.

- Claim before FRA — a permanent reduction (about 5/9% per month for the first three years early, less after).

- Claim after FRA — an 8% delayed-retirement credit per year, up to age 70.

- Past 70 — no further credit, so 70 is the practical ceiling.

It shows the math. It doesn’t tell you when to claim.

This is a deliberate line we don’t cross.

GlidePath calls the claim-age comparison exactly what it is: “a modeled comparison, not a claiming recommendation.” It will show you that, in your plan, one age leaves a larger median balance than another — and it’ll explain the break-even reasoning behind that — but it won’t say “claim at 70.” The numbers are honest; the decision is yours.

Everything happens on your own computer, from a financial file that stays local by default. The Social Security comparison is one piece of GlidePath’s retirement planning — alongside the 1,000-path Monte Carlo, the Tax Valley (your low-tax years for Roth conversions), and the ACA health-insurance bridge for retiring before 65.

Common questions.

What is a Social Security break-even age?

It’s when the larger monthly check from claiming later finally adds up to more total dollars than the smaller checks you’d have collected by claiming earlier. As a rule of thumb it lands in the late 70s between 62 and 67, and around the low 80s between 67 and 70. GlidePath shows the lifetime totals for each age and explains those ranges — it doesn’t tell you when to claim.

Does it compare claiming at 62, 67, and 70?

Yes. The Retirement page puts your benefit at 62, 67, and 70 side by side — monthly check, years collected, lifetime total in today’s dollars, and each age’s Monte Carlo success probability and median ending balance. Your full retirement age is computed from your birth year.

Does it include spousal and survivor benefits?

Yes, for couples. It models the spousal benefit (up to half the higher earner’s full amount) while both of you are alive, plus the survivor benefit one spouse steps up to if the other passes first — reduced for an early claim, the way the SSA rules work.

Will it tell me when to claim?

No. It shows the math so you can see the tradeoff clearly. What to actually do is a conversation for you and a fiduciary advisor or CPA.

Read it straight from the source, too.

GlidePath does the comparison — the official numbers come from the SSA.

- ssa.gov/myaccount — your real benefit estimate at full retirement age (the number you’d enter).

- SSA: early or delayed retirement — how claiming age changes your check.

- SSA: survivors benefits — the rules behind the survivor math.

See your own claim-age comparison.

$129 one-time for Personal, $199 for Personal + Business. Optional $39/yr keeps you current; stop any time and the app keeps working — in full, forever. Your data stays on your PC the whole time.

GlidePath Money shows you the math for educational purposes — it is not personalized financial, tax, or investment advice, and it does not tell you when to claim Social Security. Benefit figures are estimates based on the inputs you provide; confirm yours at ssa.gov. For your specific situation, talk to a fiduciary advisor or CPA.