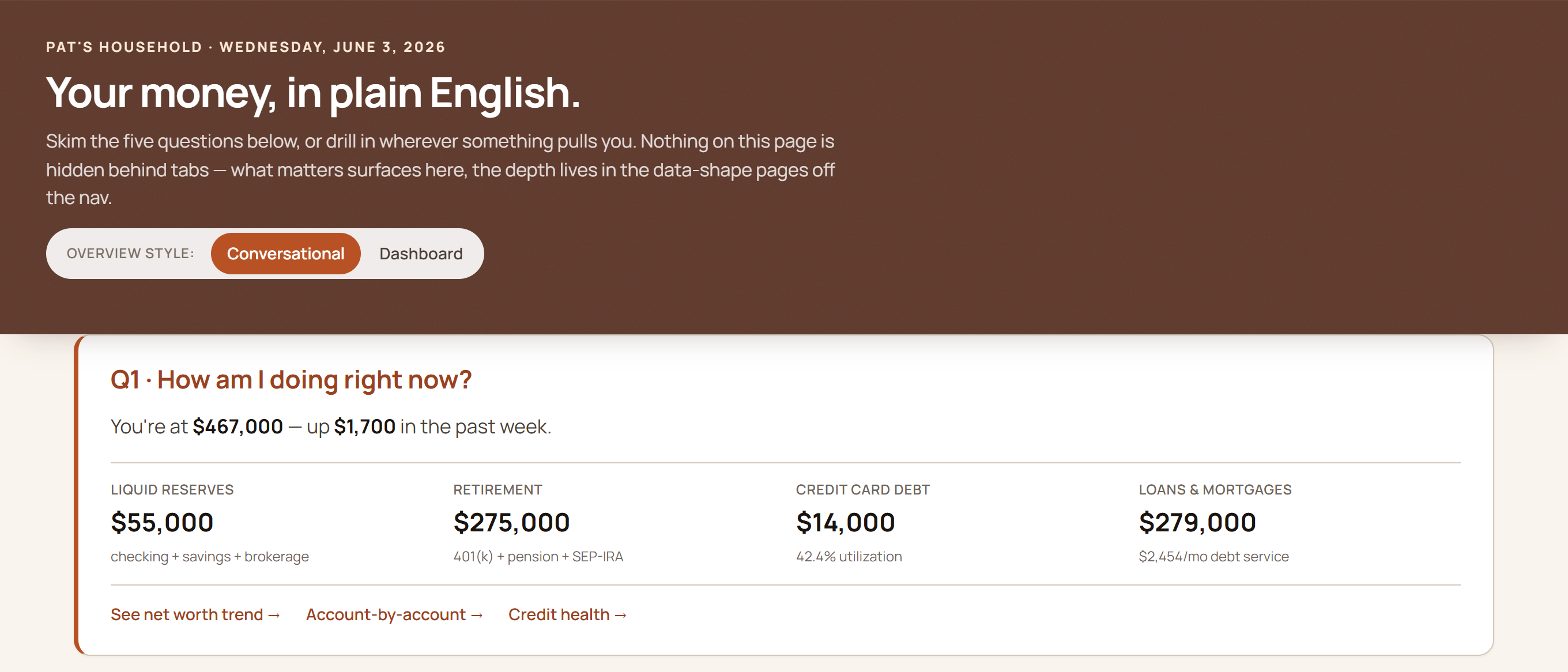

Maya Rivera — just starting out

Single, 28. Student loan, a 0% balance-transfer countdown, a first 401(k), and a house-down-payment goal.

“I finally make decent money — why does it keep evaporating?”

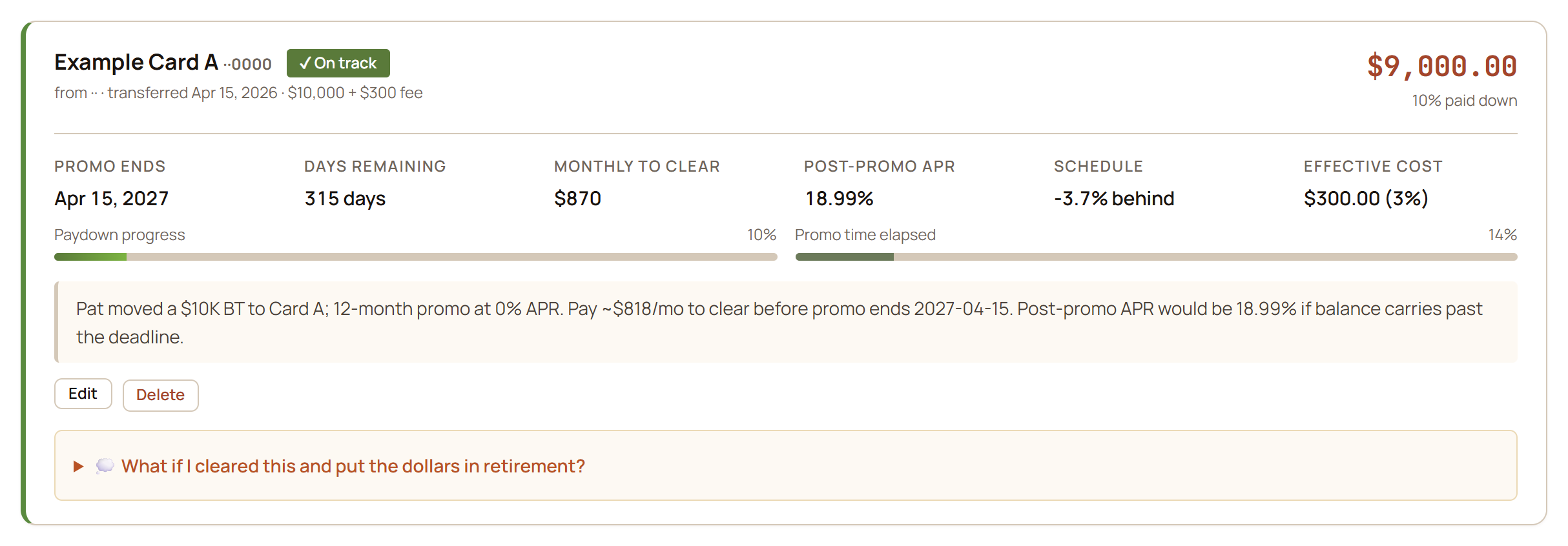

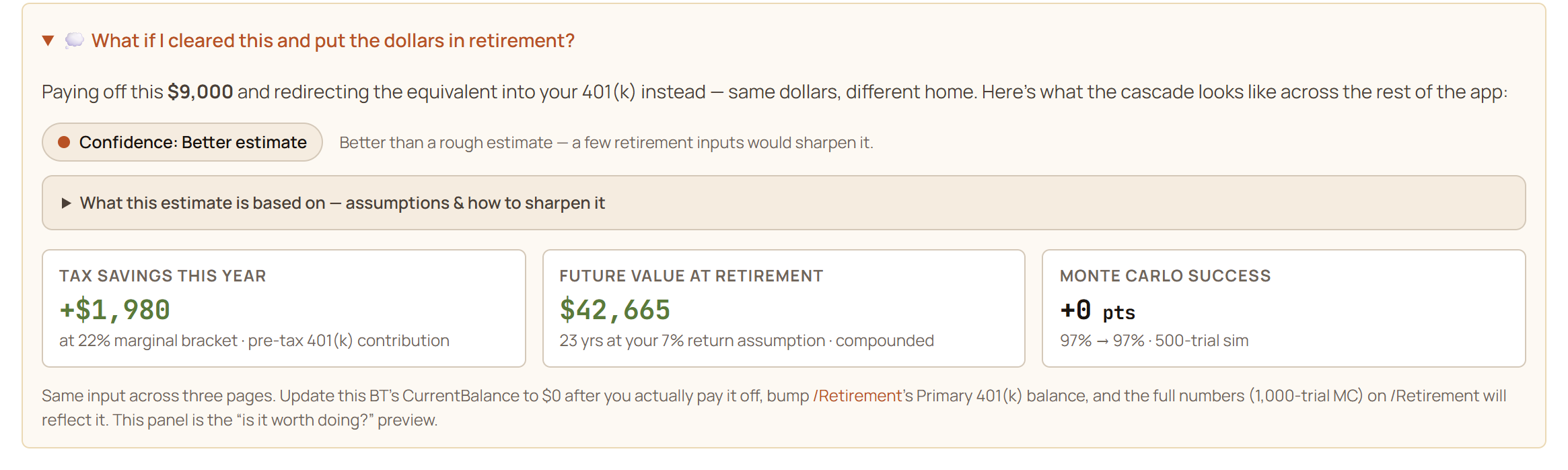

Her balance transfer has a visible deadline and a pace read — is the payoff keeping up with the promo clock? Her goals page turns “save for a house someday” into a bar that moves when her balances do, and the retirement page runs a real projection for a 28-year-old instead of telling her to come back in 20 years.

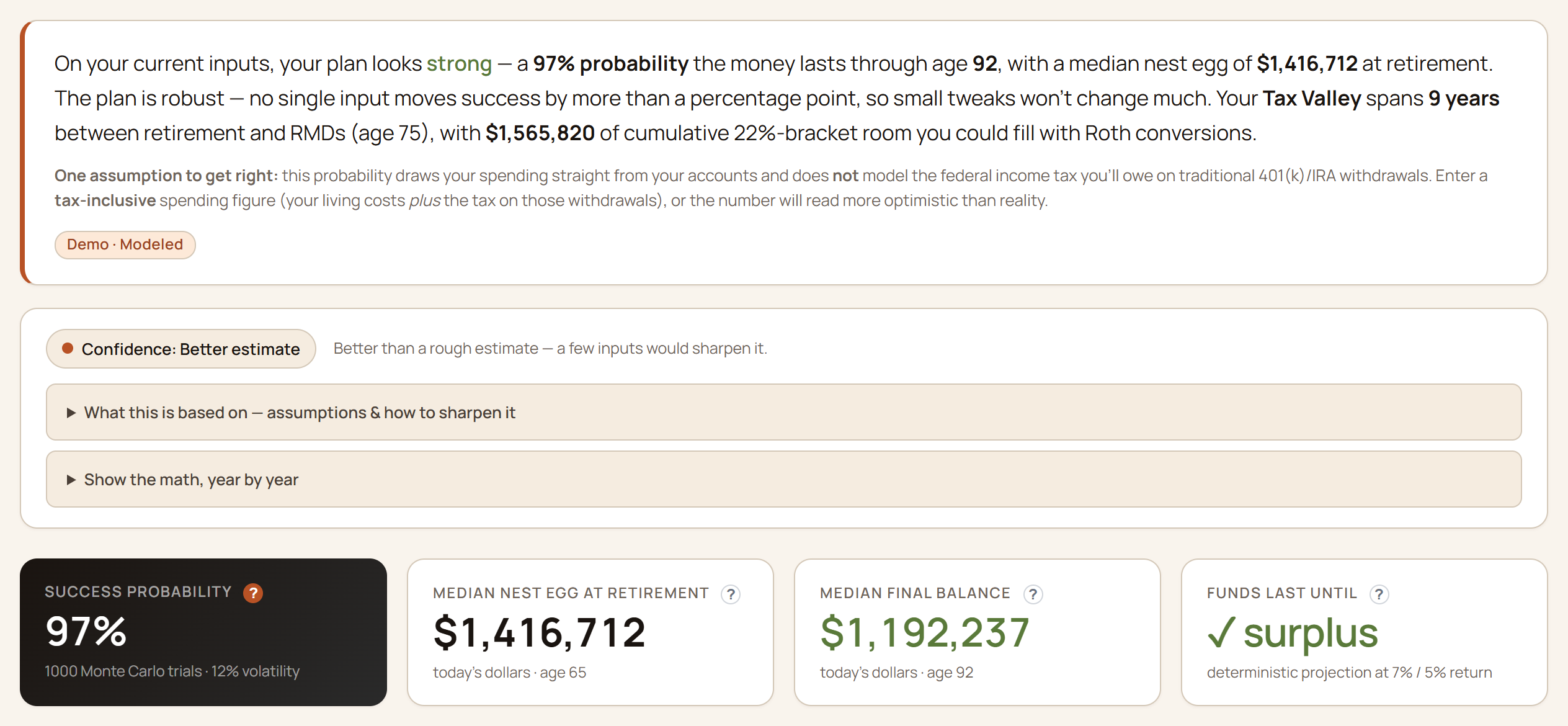

The Hwangs — almost retired

Dual-income couple, early 60s. Taxable brokerage, vested RSUs (company shares already theirs), a paid-off home.

“We saved well. When can we actually stop — and what about all this company stock?”

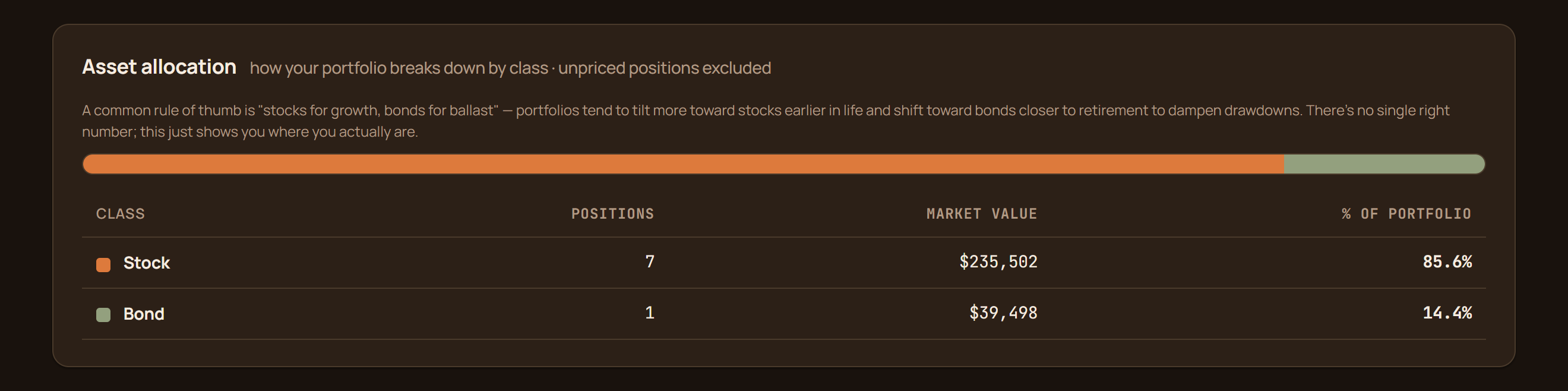

Their Tax Valley view finds the low-tax years between retiring and required withdrawals — the window where a Roth conversion (moving pre-tax retirement money to after-tax at today's rates) is cheapest to model. The ACA bridge panel prices health coverage before Medicare, and the equity pages put a number on how concentrated they are in one ticker.

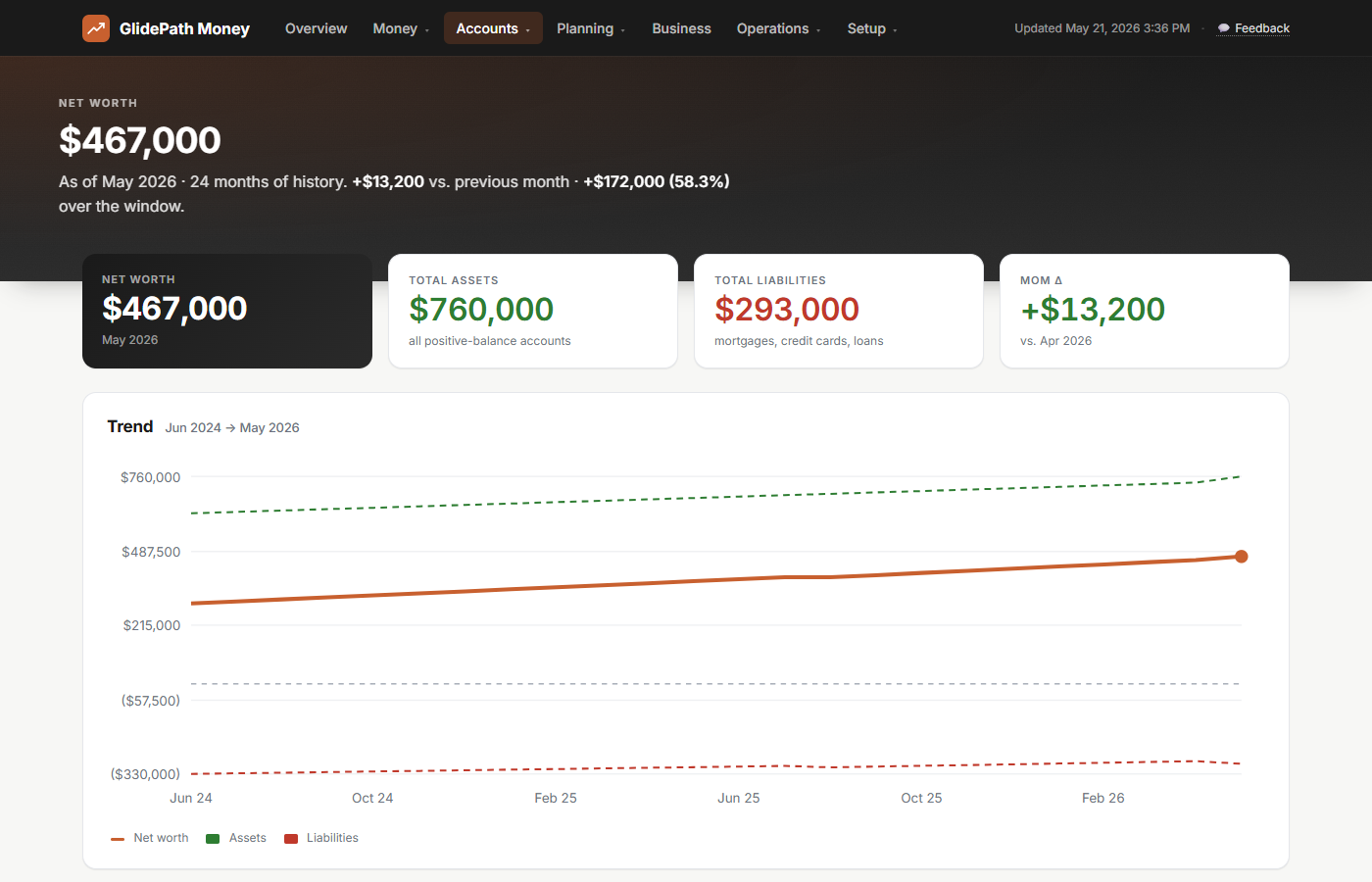

Ruth Bennett — retired & drawing down

Single retiree, 76. Social Security, a survivor pension, IRA required distributions, Medicare.

“Is the money going to last — and what does the IRS make me take out this year?”

Her required minimum distributions (the IRS-mandated annual IRA withdrawals) are computed from her actual age and balance, her drawdown runs through the same Monte Carlo as everyone else's plan, and Medicare premiums sit in the ledger as real transactions — not a footnote.

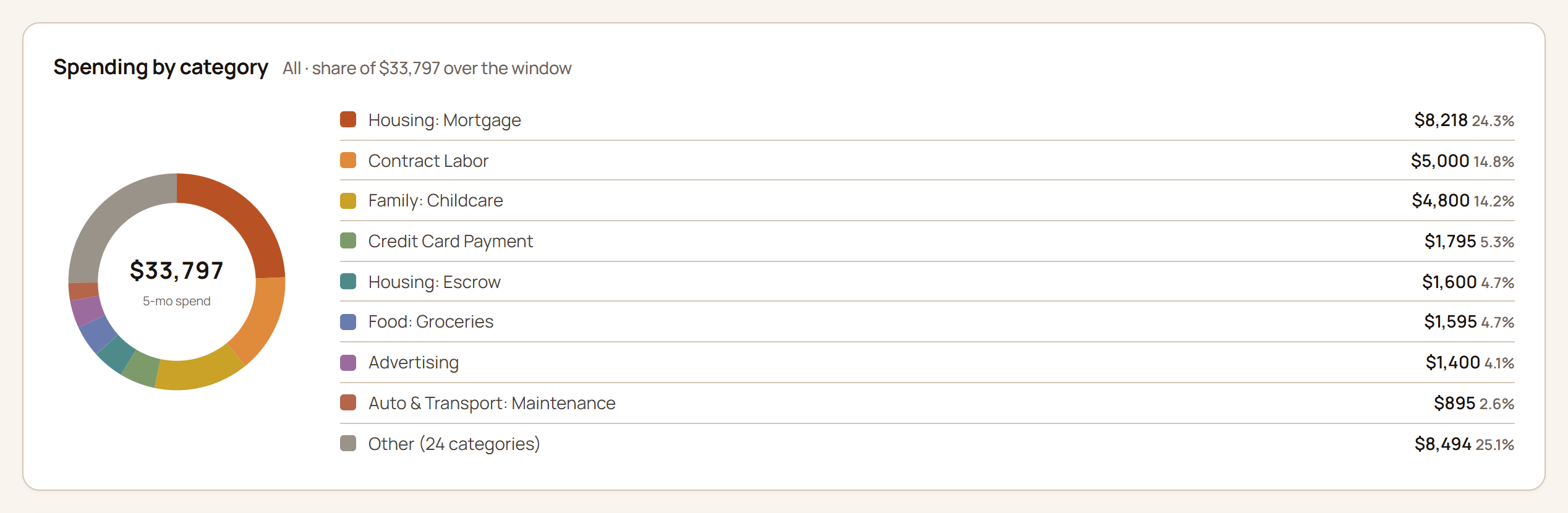

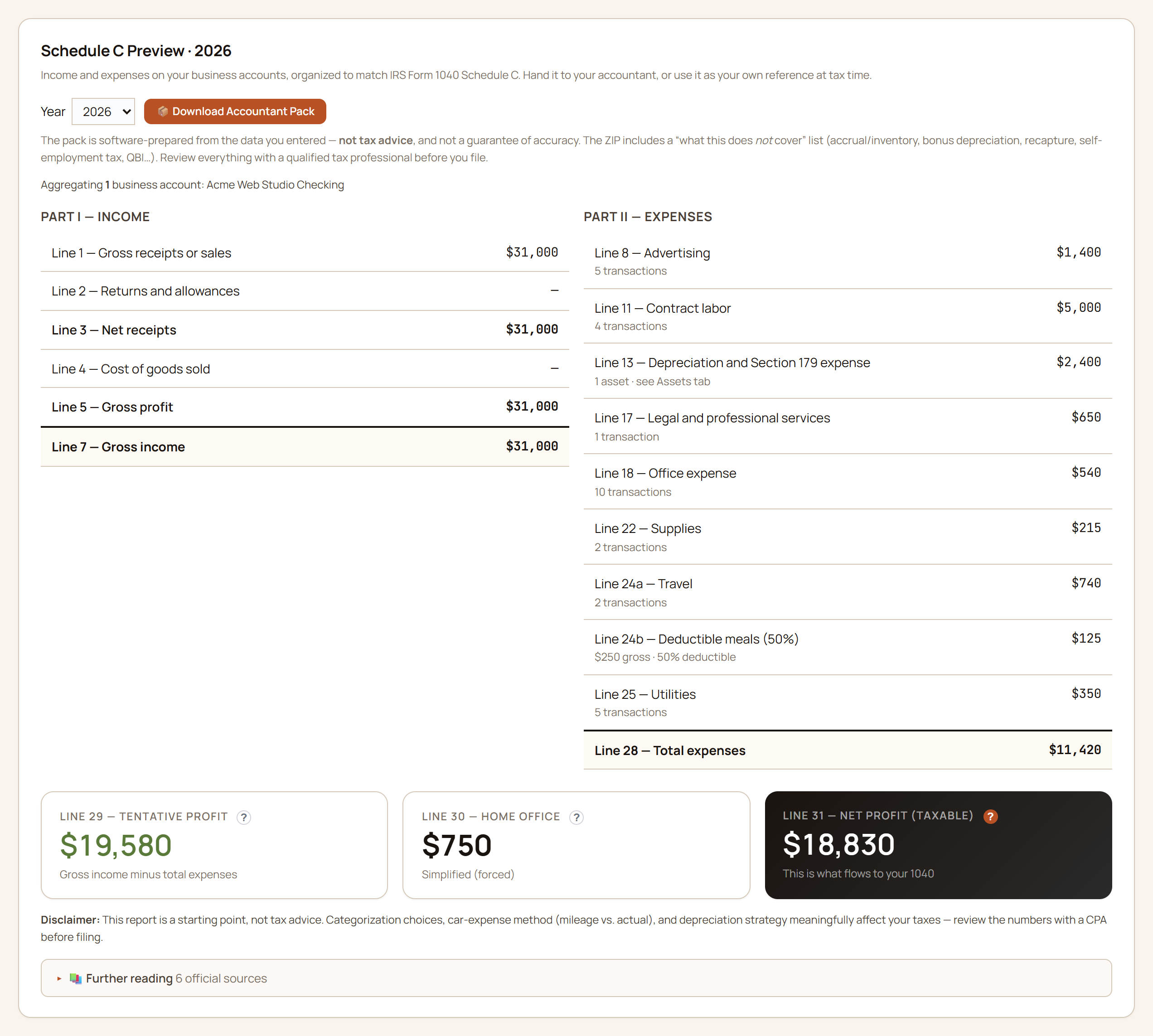

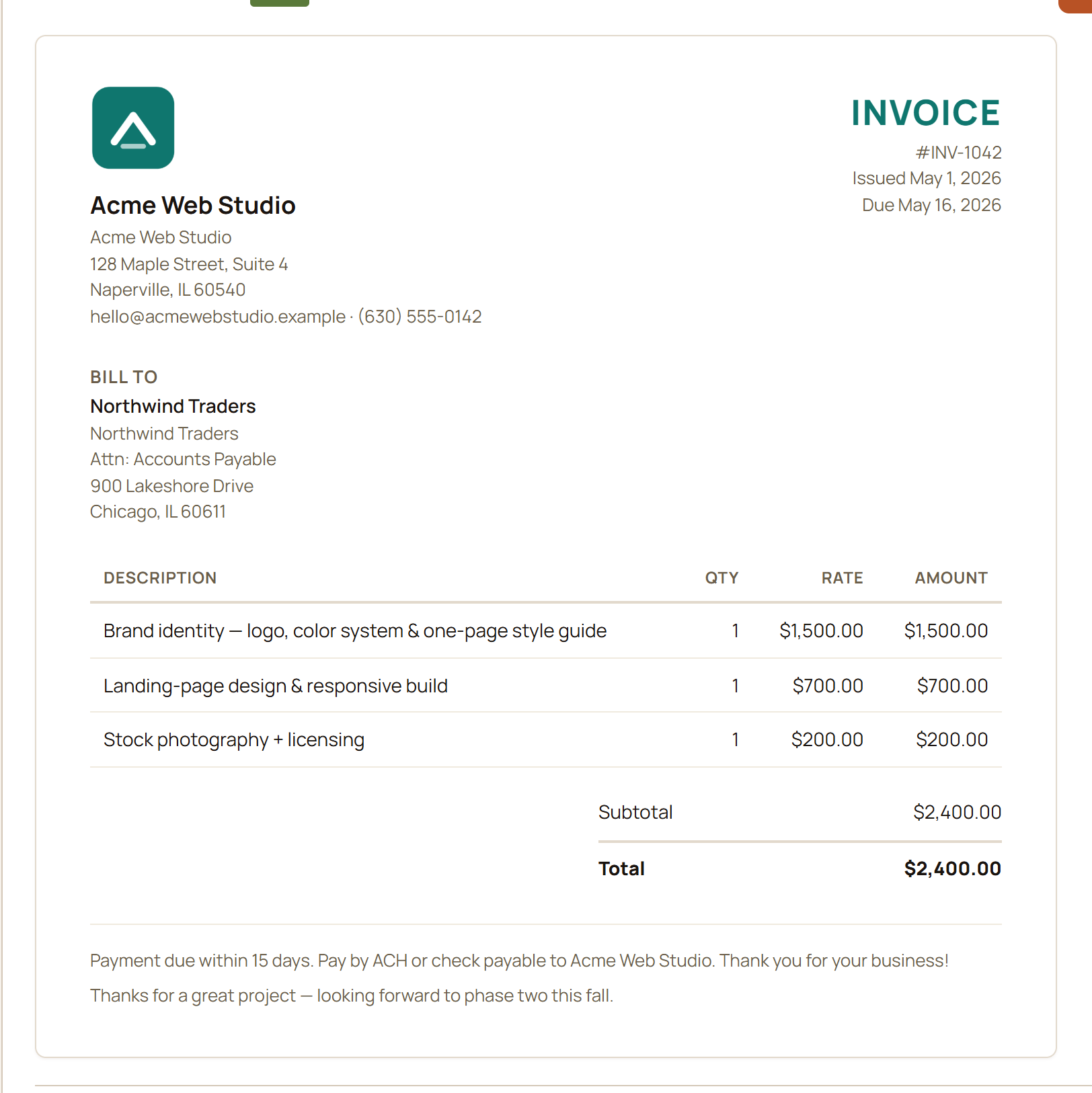

The Acme family — the everything household

Mid-career dual-income couple with kids, a mortgage, RSUs, and a freelance side-business.

“Family money AND a side business — can one app hold the whole thing without drowning us?”

The household money and the Schedule C world live side by side without bleeding into each other: family cash flow, the mortgage, and retirement on one side; invoices, deductible expenses, mileage, and a year-end accountant pack on the other. This is the household in most screenshots on this page.

All four are fictional. Each household's story is built into the app's demo data and

exercised by its automated tests, so the demo never promises a screen the app doesn't deliver.