Coming from Mint?

The Mint alternative that keeps your file local.

Intuit shut Mint down and pointed everyone at Credit Karma (which dropped the budgeting most people actually used) or a pile of monthly subscriptions. GlidePath Money is the other kind of answer: you buy a desktop license, your data lives on your own computer, and nobody can switch it off or sell what’s inside it. The difference isn't a feature list — it's the architecture.

What the Mint shutdown actually taught people.

Mint was free because the data was the product — it ran on ads and credit-card offers built from your transactions. Then Intuit retired it anyway, folded it into Credit Karma, and the budgeting features didn’t make the trip. The lesson a lot of people took away: an app you don’t pay for, that keeps your financial life on someone else’s servers, can change — or vanish — on someone else’s schedule.

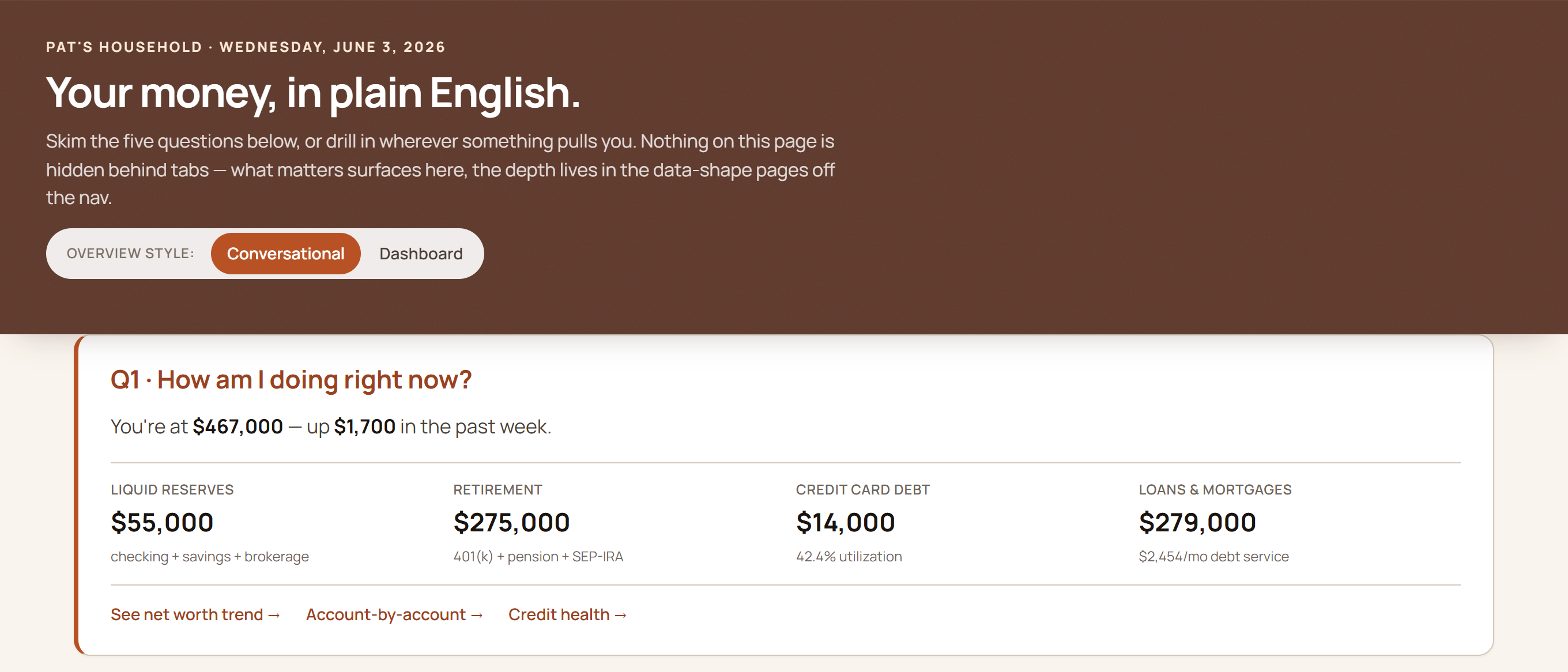

GlidePath opens to your whole picture in plain English — net worth, reserves, retirement, and debt — no ads, no “recommended” cards, nothing trying to sell you.

Computed on your own machine from plain files — the same data Mint sold, kept where only you can see it.

Three things that are different here.

A license, not locked access

$129 for Personal (or $199 with the business tools); the first year of updates is included, then $39/yr after that (auto-renews; cancel anytime). The apps Mint refugees get herded toward run $84–$109/yr when renewed annually — about $420–$545 over five years versus roughly $285 here (competitor pricing surveyed June 2026 at the lowest single-user tier; subscription prices change). Stop paying and GlidePath keeps working; the subscriptions go read-only or dark.

Your records can’t be shut down on you

GlidePath runs on your computer and stores everything as plain files you can open in any spreadsheet. Even if a license ever stopped working, those files would still be sitting right there on your disk — nothing on someone else’s server to lock, migrate, or shut down.

You’re the customer, not the product

No ads, no “recommended” credit cards, no data monetization. Because it’s local-first, your transactions stay on your machine by default, and the optional cloud features each show exactly what they send before you use them. You paid for it, so it works for you.

The honest tradeoff.

Mint auto-synced everything. GlidePath doesn’t — and that’s deliberate.

Mint connected to your banks through an aggregator and pulled transactions automatically. Convenient — but the numbers arrived through a standing connection you did not control. GlidePath brings data in two reviewable ways:

- A free browser extension that captures your download in one click on Chase, American Express, Citi, and Bank of America (more coming).

- Drag-and-drop CSV import for every other bank (plus PDF statement import for Chase, American Express, and Bank of America).

It trades set-and-forget for a few minutes of your attention. But your financial file stays local by default — and a ten-minute monthly check-in you actually do turns out to be the part that changes habits, not the part to automate away.

And things Mint never did.

Mint was a rear-view mirror. GlidePath looks forward too.

Retirement projections that run your plan through 1,000 market futures. Your Tax Valley — the low-tax years after you stop working when Roth conversions are cheapest. Countdowns on 0% balance-transfer promos before the rate snaps back. And Glide, an in-app helper that answers “what does this number mean?” in plain English — without ever seeing your accounts. See the planning depth →

Bring your Mint history.

You don’t have to start from zero.

If you exported your transactions from Mint before it closed, drop that CSV onto GlidePath’s Import page — format auto-detect reads it and your history comes right along. Years of categorized spending, picked up where Mint left off.

Ready to leave the subscription treadmill?

$129 for Personal, $199 for Personal + Business. First year of updates included, then $39/yr keeps eligible tax rules, parsers, security fixes, and features current (auto-renews; first charge about a year after purchase) — cancel any time and the version you already have keeps working.

GlidePath shows you the math — for your specific situation, talk to a fiduciary advisor or CPA.