RSUs can become real money. They can also disappear before they vest.

That tension is why unvested restricted stock units should not be treated like guaranteed retirement income.

If you work for a company that grants RSUs, the numbers can be large enough to change your planning picture. Upcoming vests may affect taxes, cash flow, concentration risk, and how much employer stock you eventually hold. Ignoring them completely can make the plan feel incomplete.

But counting every scheduled vest as guaranteed money can make the plan too optimistic.

The safer answer is not “ignore RSUs.” It is “separate vested from unvested, then model unvested shares as a scenario.”

Vested and unvested are different kinds of money

Vested shares are shares you have already earned. If you still hold them, they belong in net worth. They may also create employer-stock concentration risk. If you sell them, your cost basis (what the IRS treats as your purchase price — usually the share value on the day they vested) and the resulting gain or loss matter.

Worth knowing how that lands in GlidePath, because it isn’t automatic: tracking a grant does not add its value to net worth. Vested shares count once you enter the brokerage account holding them as an account, like any other balance. The Equity page tracks grants, vesting and concentration on its own — deliberately separate, so shares already sitting inside a brokerage balance you entered can’t be counted a second time. The trade-off is that a grant you never mirror as an account is visible on the Equity page and absent from your net worth.

Unvested shares are scheduled future compensation. They depend on employment, vesting rules, company performance, stock price, and taxes at vest. They may be valuable, but they are not cash in the bank.

A clean RSU model should answer both questions:

- What do I already own?

- What might vest later if assumptions hold?

Those should not be mixed into one number without a label.

Why base plans should be conservative

A retirement base plan should be the version you can trust without giving uncertain future compensation the benefit of the doubt.

That means the base plan should usually exclude:

- unvested RSUs

- future bonuses

- future job changes

- inheritances

- expected spending cuts that are not already true

- future home-sale proceeds unless explicitly entered

The base plan is not pessimistic. It is disciplined.

It says: “Given what is already in the household financial picture, what does the projection show?”

Then the RSU scenario can ask: “What changes if these scheduled vests happen and the stock is worth the current assumed price?”

That second question is useful. It just should not silently become the default.

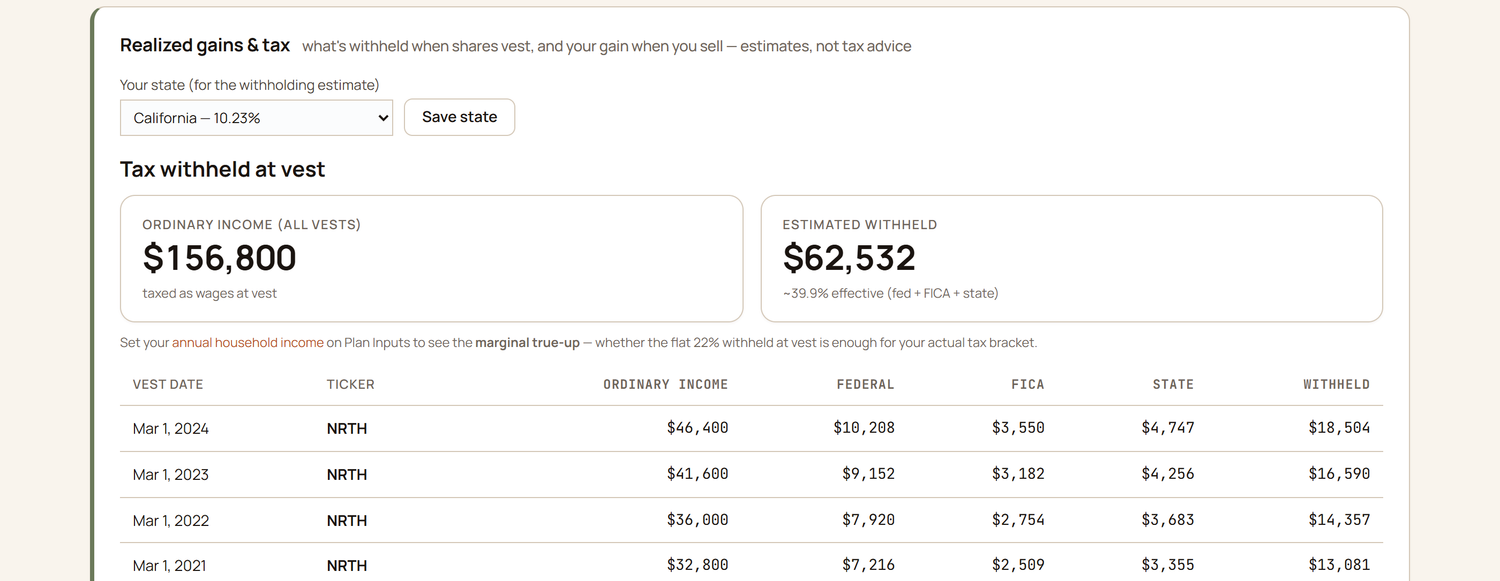

The tax wrinkle

RSUs are taxed as ordinary wage income when they vest. The vest-day fair market value matters because it becomes the income amount and typically the basis for shares delivered after withholding.

That means two people with the same number of unvested shares can have very different outcomes depending on stock price, withholding, tax bracket, state, and whether they sell or hold.

A planning app should be careful here. It can estimate and explain, but it should not pretend RSU tax outcomes are certain or personalized tax advice.

Useful RSU fields include:

- grant date

- vest date

- shares scheduled to vest

- fair market value at vest

- shares withheld

- shares delivered

- cost basis

- sale price, if sold

- current price for held shares

The more of those fields you have, the more honest the view can be.

Concentration risk matters too

RSUs create a second question beyond income: how much of your financial life depends on one employer?

If your paycheck, bonus, unvested RSUs, and a large part of your portfolio all depend on the same company, the household is concentrated. That may be intentional. It may also be a risk worth seeing clearly.

This is not a software decision. It is a human tradeoff.

A good tool should show:

- vested employer stock value

- unvested value, separately labeled

- percent of investable assets tied to employer stock

- what changes if the stock price moves

- whether unvested shares are excluded from the base retirement projection

That is more useful than burying RSUs in a generic investment total.

How GlidePath handles RSUs

GlidePath separates RSUs into household planning pieces:

- vested shares held

- unvested shares still scheduled

- upcoming vest dates

- current prices

- employer-stock concentration

- estimated tax at vest

- retirement base plan versus optional RSU-upside scenario

The important phrase is optional scenario.

GlidePath’s base retirement projection keeps unvested equity out by default. If you want to see the upside case, you can compare what changes if the scheduled vests land and you bank them. That comparison is useful because it shows the modeled effect without pretending the future has already happened.

It also gives you a better conversation starter for a tax pro, advisor, or spouse:

“Here is the base plan. Here is what changes if the RSUs vest. Here are the assumptions.”

That is safer than letting unvested compensation quietly inflate the headline plan.

A practical rule of thumb

Use three buckets:

- Vested and held: count in net worth — in GlidePath, by entering the brokerage account that holds them, not by logging the grant.

- Vested and sold: track proceeds, basis, and gain/loss.

- Unvested: keep out of the base plan; model as upside or separate compensation.

That does not mean unvested RSUs do not matter. They may matter a lot.

It means your plan should stay honest about what is already yours and what is still conditional.