A 0% balance transfer can feel like breathing room. The interest stops for a while. The monthly statement looks calmer. The emergency is no longer screaming.

That is useful. But it can also hide the real problem.

The balance is not the whole story. The promo end date is the cliff.

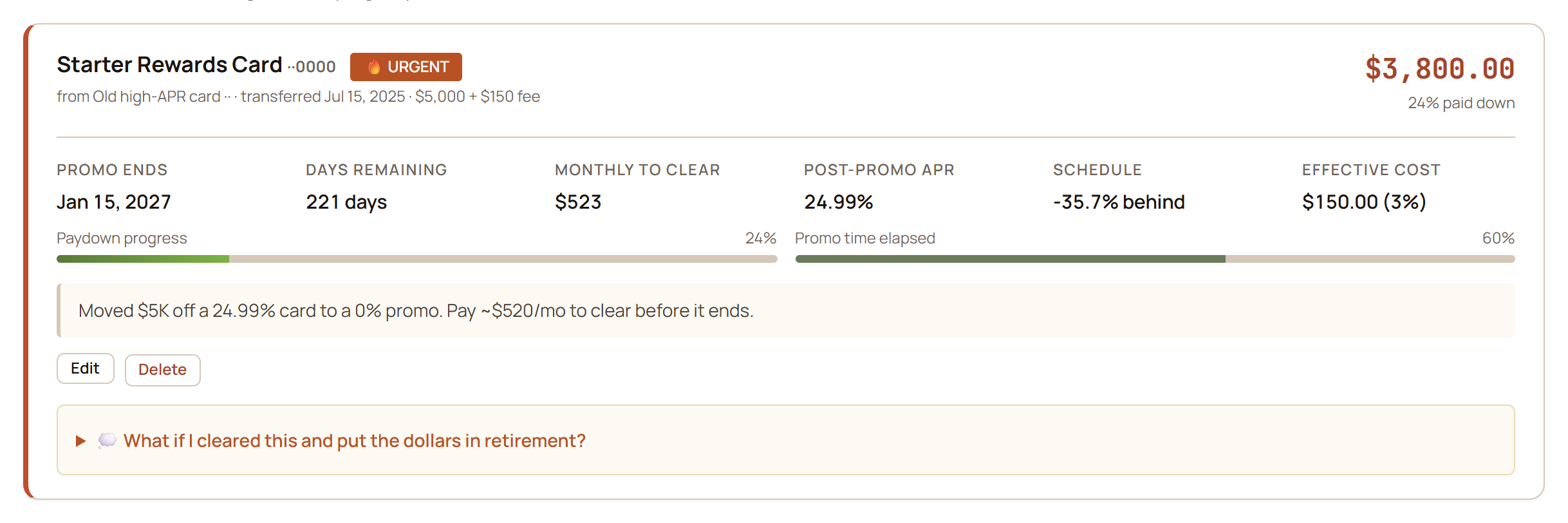

If a card has $6,000 left and the 0% period ends in 15 months, the tracking question is not just “What do I owe?” It is “How much do I need to pay every month to reach zero before the rate jumps?”

That number is the clear payment.

The minimum payment trap

Minimum payments are designed to keep the account current. They are not designed to guarantee that a promotional balance clears before the promo expires.

Suppose a transfer has:

- $6,000 current balance

- 15 months remaining

- 24.99% post-promo APR

- $150 minimum payment

The simple clear-payment math is:

$6,000 ÷ 15 months = $400 per month

If you pay only $150, the card may look “handled” because the statement is current. But the promo is falling behind by about $250 per month.

That is the gap GlidePath cares about.

What to track for every balance transfer

For each promo, write down six fields:

- Transfer date

- Original transfer amount

- Current balance

- Promo end date

- Post-promo APR

- Transfer fee

The transfer fee matters because 0% is not always free. A $10,000 transfer with a 5% fee costs $500 immediately. Whether that is worth it against the interest you would otherwise pay is your call — but it is a real cost to weigh, not zero.

The post-promo APR matters because the first month after the cliff can be expensive. If a large balance remains when the promo ends, the card starts acting like ordinary credit-card debt again.

The promo end date matters because the same balance can be fine or risky depending on time left.

The three numbers that make the risk visible

Once the fields are in place, three numbers tell the story.

1. Monthly to clear

Current balance divided by months remaining.

This is the monthly amount that would bring the balance to zero by the promo end date, before considering new charges.

2. Schedule gap

Compare paydown progress to time elapsed.

If the promo is 50% over and the balance is only 20% paid down, you are behind schedule even if the card is current.

3. Cliff cost

Estimate what happens if the promo ends with a balance still on the card.

The useful version of this has two parts. First, the balance you would actually reach — not the balance today, but what is left at the promo end if your current pace continues. Second, what that leftover costs once the promo rate expires: the first month of interest at the post-promo APR, and the interest carried over a full year if the balance keeps sitting there at the same pace.

Those two numbers are what turn “later problem” into “visible cost,” because they answer the question a balance alone cannot: is the pace I am on good enough, and what does it cost me if it is not?

Why calendar reminders are not enough

A calendar reminder 30 days before the promo ends is better than nothing. But it is usually too late to change the outcome.

If a card has $4,000 left and the reminder arrives one month before the cliff, the clear payment is $4,000. That is not a reminder; it is a surprise.

Better reminders happen in layers:

- 180 days out: is the current pace working?

- 120 days out: does the monthly payment need to change?

- 90 days out: is this now an urgent item?

- 30 days out: confirm payoff or move the plan to “what happens after the cliff?”

The goal is not panic. The goal is enough notice that the payment plan is still realistic.

What GlidePath does differently

GlidePath’s balance-transfer tracking is built around the cliff, not just the balance. It can show the promo end date, days remaining, monthly-to-clear amount, schedule status, the fee-inclusive cost of the transfer, the balance projected to be left at the cliff at your current pace, and what that leftover would cost in interest — both the first month and a full year of carrying it.

It also puts those dates next to other household obligations. A promo date competes with bills, subscriptions, loans, tax deadlines, and Monthly Close. Seeing the date in context is more useful than seeing the balance alone.

GlidePath does not tell you which debt choice is “best.” It shows the balance, date, payment gap, and post-promo exposure. A separate retirement fold compares your recorded plan with one card-balance-sized bump to the primary 401(k) starting balance; it does not simulate clearing the card or redirecting the freed-up payment.

A simple balance-transfer review

Once a month, ask:

- Did the current balance go down?

- Is the clear payment still affordable?

- Is the schedule gap improving or worsening?

- Did the promo end date change or get entered incorrectly?

- Is the post-promo APR known?

- If this is paid off, where will the freed-up payment go?

That last question matters. Paying off the transfer is the first win. Deciding what happens to the freed-up monthly payment is the second.

It might rebuild cash. It might go to another card. It might increase retirement contributions. It might simply create breathing room.

The right next step depends on the household. The useful software job is to make the cliff visible early enough that the decision is not forced by surprise.